Tighter funding and rising costs push the kingdom’s wealth fund to reposition itself as a capital partner rather than a capital source

Saudi Arabia’s Public Investment Fund is entering a different phase. The numbers still point to scale, with assets expected to reach $2 trillion by 2030, but the strategy behind that growth is shifting.

The new 2026–2030 framework marks a clear move away from a model built on deploying sovereign capital at speed. Instead, the fund is repositioning itself as a platform designed to attract, structure and recycle capital. This is less about slowing down and more about changing roles.

Pressure builds beneath the surface

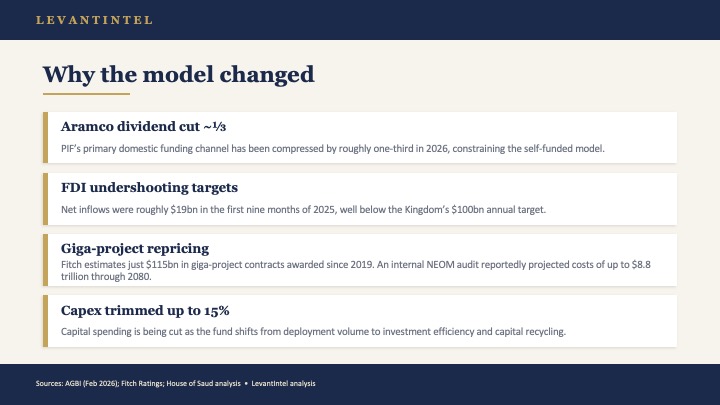

Aramco’s dividend, a key funding channel, has been reduced. Foreign direct investment remains below expectations, with inflows falling well short of the kingdom’s $100bn annual target. At the same time, large-scale projects have become more expensive than initially projected.

The combination has forced a rethink. Capital is no longer treated as unlimited, and the focus is moving towards efficiency and return.

A different kind of engine

The new structure splits PIF into three portfolios.

A domestic “Vision Portfolio” continues to anchor economic transformation across sectors such as logistics, manufacturing and clean energy. A “Strategic Portfolio” focuses on scaling national champions, including emerging areas like artificial intelligence. A “Financial Portfolio” provides diversified global returns.

Together, they create a more disciplined framework. Deployment is no longer the goal on its own, returns and sustainability carry more weight.

From capital provider to capital broker

The most important shift sits in how PIF interacts with global capital. Through co-investment structures, loan guarantees and a growing IPO pipeline, the fund is positioning itself as an anchor investor rather than the sole financier. Risk is being shared, and in some cases absorbed, to attract institutional partners.

PIF is no longer just writing cheques, it is structuring deals.

This is not a retreat, it is a readjustment shaped by tighter funding conditions and more demanding capital markets. For investors, Saudi Arabia remains open, but the terms are evolving. The next phase will depend less on how much capital PIF can deploy and more on how much it can attract.